[Market Madness] Special News Briefing 001

From my desk, to yours

Fellow Readers,

I’ve been kicking the can down what seems to be the longest road ever. Although I like the new monthly recap format, I lose some of the creative freedom I had in the earlier editions. So, you may be wondering why I migrated in the first place. Well, it was easy, and it allowed me to continue the cadence of writing and publishing with little backlash and sleepless nights to get more frequent content out there.

I’ve launched this ad-hoc publication to supplement the monthly recaps. When there is something worth putting the pen to, I will do that here. Today, I have a hodgepodge of ideas that I will spill out and hope to tie it all up in a nice bow by the end. The road is winding but bear with me.

There is a lot going on in finance. So much so, I hardly recognize the profession I dreamed about as a young collegiate. For all that is new to me (spacs, meme stocks, crypto, defi, etc.) so much is still the same. Banking is still banking, and capital markets are still capital markets.

In my heads down, read as much as I can journey, I’ve come to map our current point in time as a historically significant crossroad. The significance of democratization, politicization, and isolation have led to significant deviations in what was standard.

Where we are with finance and economics

I’ve seen this quote enough this past year that it has almost become a theme: “It's just that the investment banking profession will sell shit as long as shit can be sold.” I’d argue that this can be expanded to fit the finance world at large, but the idea still stands, ever since 2011.

The world of “special situations” has really grown interesting to me. For those unaware, this area specifically focuses on companies in distress (in the stages before or after filing for bankruptcy). The team over at PETITION are keeping it real. A recent post was really thought provoking to me.

Coupled with the below tweet (with OP here), we see a real-life interpretation of scraping the bottom of the barrel for the last ounce of yield:

We’re seeing so much movement further out the yield curve, that investors (retail/institutional/hedge fund or otherwise) are buying into junk debt at such a pace that those yields are within 100 bps of U.S. government debt… let that sink in.

As we consider what could be evolving into a toxic cesspool, the debt market is flush with cash, thanks to the Fed and investors looking to capture additional return for seemingly equitable risk.

From there, we move on to the interplay between the Fed and the Capital Markets. Who wouldn’t want to have issued debt in the last 12 months? The Fed has essentially backstopped the corporate debt market, providing near immunity to even the riskiest balance sheets. The Reverse Repo (RRP) market is still going hot too.

Many are struggling to make sense of the Fed comments. We have hawkish statements, with underlying dovish actions, and conflicting reports across the bank presidents, especially the non-voters.

Then, we get to the topic of inflation. At this point it is everyone’s conversation starter among the financial community. I’ll lead by saying I don’t know if the current wave is transient or not. I see the Fed running inflation hot as they focus on closing the unemployment gap from pre-pandemic levels.

The same stimulus that helps also hurts. The unemployment recovery is challenged by the continued UI (unemployment insurance) benefits that some states are yet to phase out. On the backend, workers are then demanding higher wages to incentivize them to put the remote down and return to work. Higher wage demands lead to cost increases, and so the cycle continues. The early data today, with weekly claims tomorrow, suggest that the labor market is plateauing, or even declining, putting a damper on general economic expectations.

The other side of the coin for inflation is the topic of supply chain constraints. Large-scale manufacturing is not so good at starting and stopping at a moment’s notice. With the addition of technological advancements that gave way to “just in time” inventory management, inventory backlogs grew to nothing very quickly in the wake of the pandemic and the current wave of rejuvenated demand for goods that cannot be made quickly, i.e. cars.

A final note on special situations and selling garbage… SPACs. Currently, I am struggling to put together this market. I see considerable risks in the go-to-market space as compared to direct listings and IPOs. My concerns fall in the timeline. This is not to say that all companies going public through SPACs are bad companies. But just because you have an easier in to go public, does not mean that the company should go public. The rushed timeline and lucrative incentive structure make me skeptical about the longevity of SPACs. Appetite for new companies is present in the market right now, as the influx of retail investors and increased market access.

This appetite is concerning me for several reasons. For some of these ‘hotter’ names, there is absolutely no way to justify the valuation to the market pricing. If the pricing is way above the valuation, then what’re you paying for? Goodwill? Future expectations are technically already priced in when a valuation gives you a per-share value.

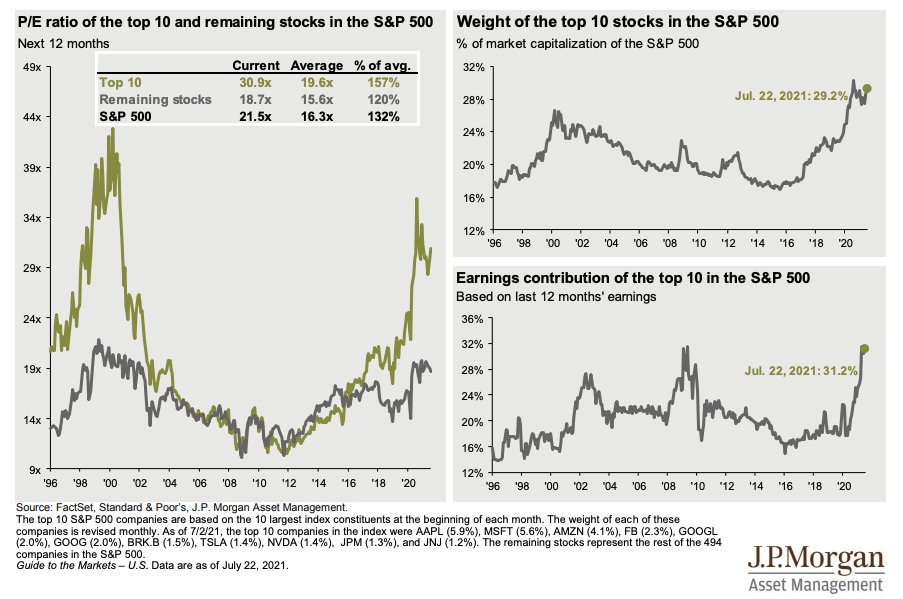

Narratives and hype seem to be holding firm, at least for the time being in the equity capital markets. What scares me is that I’m hearing from a lot of angles that market breadth is shrinking, P/E’s continue to extend (somewhat unreasonably), and if the economy rolls over, then these recent IPOs and valuations are going to drop precipitously if there aren’t cash flows backing it up.

Tying it up

What did this whole essay try to convey? The markets are pretty tangled out there. The stimulus high is wearing off, the labor market is plateauing, and the deviation between market prices and fundamentals seems to remain wide. If this was a confusing piece, that was partly on purpose. I’m trying to convey the idea that all the above items are in play at once. The fog is heavy, and the road ahead is anything but clear.

Rates are going to have to move up at some point, whether the market likes it or not. We need investors to retreat towards the safer end of the risk curve, and we need to see money market funds get some reprieve.

Long story short, we’ve got a long way to go.

A palette cleanser on defi

I’ll spend more time in the future working out my feelings on and understanding of the DeFi space, but I will share some thoughts that I’ve come to along the way:

Behind the veil of the memes and the concerns over malpractice and misuse, there is potential there. This Tether thing has me understandably concerned, but who wouldn’t be (below video clip for context).

There is definitely a lot of optimism and potential in the space, and I support that. After all, there are at least 12 companies looking to be the first to bring a BTC ETF to market (and likely other coins/tokens to follow suit after one is successful). It is also worth mentioning that there are dozens and dozens of new companies that are developing options platforms, liquidity pools, and yield farming investments to continue building out a robust defi infrastructure.

Additionally, for what it is worth, Premia Finance has some incredible press art.

Finally, happy birthday Onramp! Cheers to many more. Your spot in the Journal is kick-a$$!