[Market Madness] June 2021 Edition

A sampling of financial delights

What’s new

Administrative topics and an introduction

Well folks, I got a lot of positive feedback regarding the last edition, which is very nice!

This edition, I am going to do the same, and highlight a handful of posts that I’ve made over on Bookshlf, highlighting a palette of topics that I’ve been paying attention to. Additionally, I end this month’s post with some longer articles and papers I’ve been making my way through more recently.

This week, we talk about:

EVs

Donuts

Labor Market Data

Commodities

SPACs

The Post-Pandemic Debt Hangover

and…

The Economic Question of Our Time

Did you miss the last edition? No worries! Get it right here and catch up on the madness.

What’s been on my radar

Below are some posts I’ve made on Bookshlf (oldest to newest) that highlight some of the bigger picture topics that I have been paying attention to over the past weeks.

Ford EF-150

Ford appears to be on track to be a strong force in the EV space. In past posts, I've expressed my dissatisfaction with Tesla and the EV space as it stands currently. I do think that Ford has what it takes to pivot in the market and be a strong, US-based auto manufacturer that will bring EVs to the affordable market for US consumers.

Notable Quote: "Ford said it plans to boost spending on electric-vehicle development to $30 billion by 2025, roughly one-third more than it forecast earlier this year. The increase in spending—a total that includes some money spent in the past few years—is driven by Ford’s plans to eventually begin manufacturing its own batteries, including at two future U.S. battery-cell factories, with Korea’s SK Innovation Co."

Krispy Kreme’s new IPO

New IPO Alert: Krispy Kreme ($DNUT) filed to go public today via an IPO. But this is not the first time the company has gone public. Their first IPO launched in 200 on the NASDAQ under ticker $KKD. They were taken private in 2016 "by European conglomerate JAB Holding at a $1.35 billion valuation. JAB also owns Panera Bread, Caribou Coffee, Au Bon Pain, and Pret A Manger. The S-1 filing suggests that JAB would remain the controlling shareholder."

The company reported a net loss in 2020, suggesting that COIVD impacted the company hard. They had reported $1.12 billion in topline revenue, but a bottom-line net loss of -$60.9 million. Their public filing could be due to an additional source of fund raising outside of debt.

DNUT's S-1 Filing with the SEC

Lukewarm Jobs Report (May BLS Recap)

Today (June 04) was a big day for the US economy; it was a 'lukewarm disappointment' as the NFP report came in high, but still below what was expected. The US economy added 559,000 jobs in May, coming shy of the 670,000 jobs that were expected.

Markets reacted positively to the labor market news, despite coming under expectations. There are some suggestions here that this could be a goldilocks situation, coming in not quite over the top, but also not too low that concerns were risen... just right.

I do suppose that this report was a net positive for the economy, showing that the labor market is continuing to add new jobs, but also not running too hot nor too cold.

Cost Pressures

A lot of interesting things are happening in commodities right now. We're seeing a challenging overlap of different circumstances and one of the fastest revitalizations of the global economy following a market downturn. The collapse, shutdown of global supply chains, mixed with the speedy reopening and continued strain on supply chains is causing a great deal of pressure on suppliers and producers. All this leads to one thing that many continue to fear: inflation.

Notable Quote: "The world hasn’t seen such across-the-board commodity-price increases since the beginning of the global financial crisis, and before that, the 1970s. Lumber, iron ore and copper have hit records. Corn, soybeans and wheat have jumped to their highest levels in eight years. Oil recently reached a two-year high… Many factors are driving the increases, including ultra-strong consumer demand and supply-chain bottlenecks. But behind many of them, many economists say, is a deliberate decision by policy makers in the U.S. and elsewhere to run their economies hot for now, with lots of stimulus, to ensure they recover fully from damage caused by Covid-19."

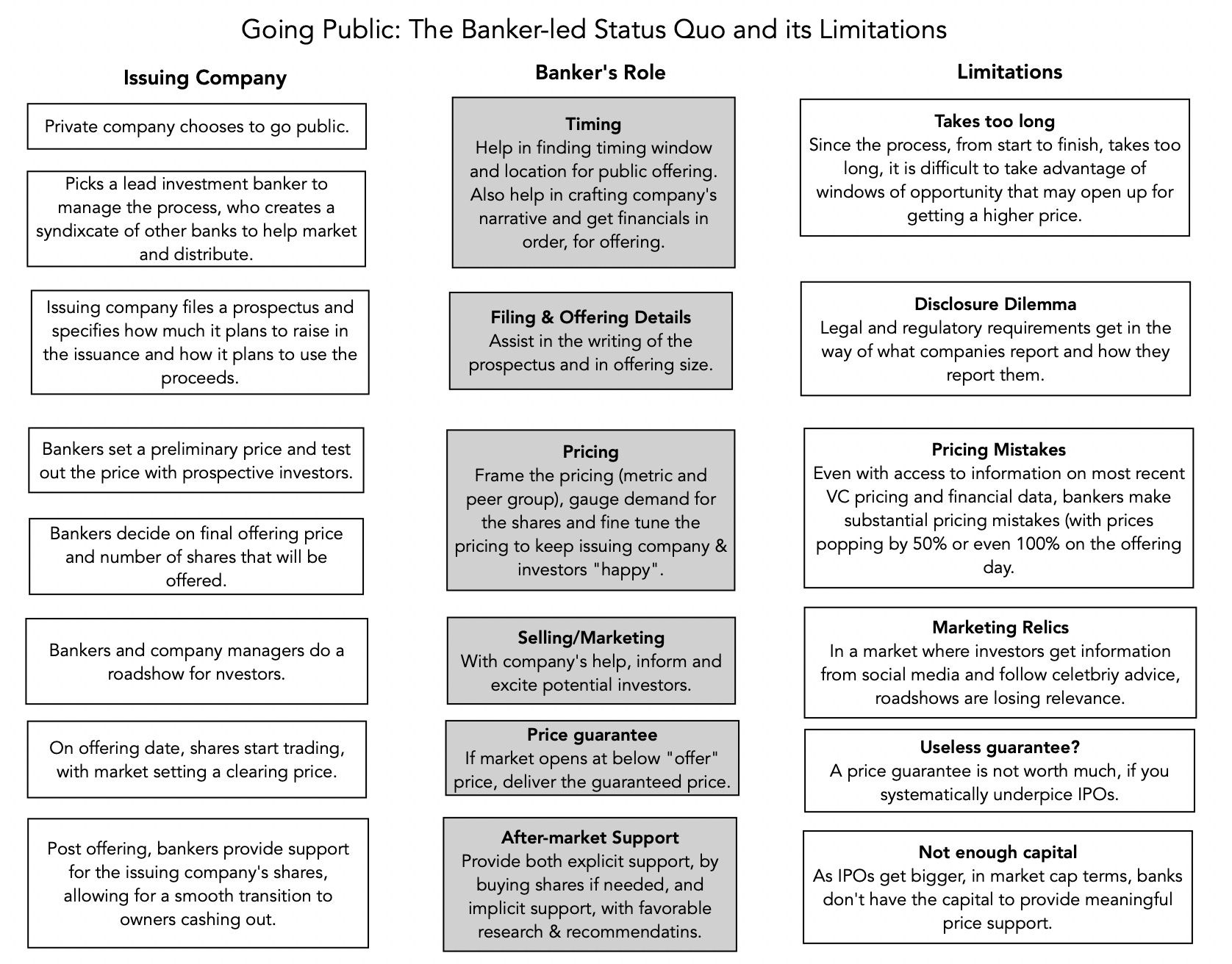

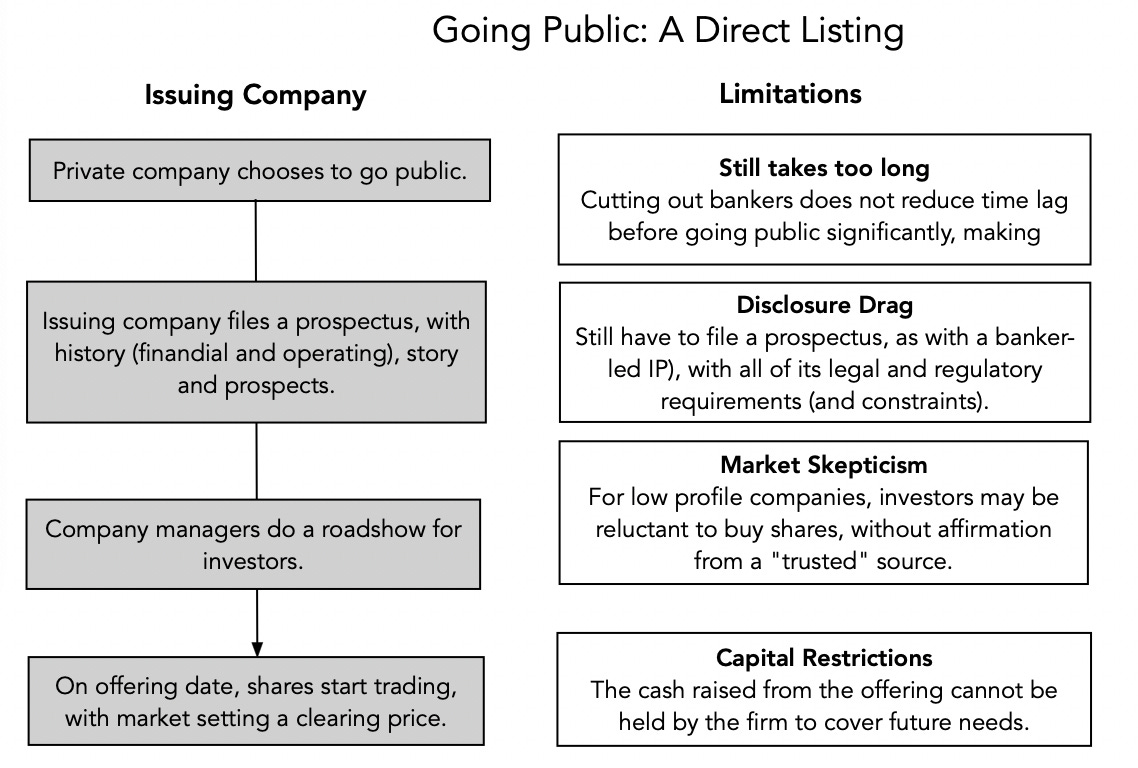

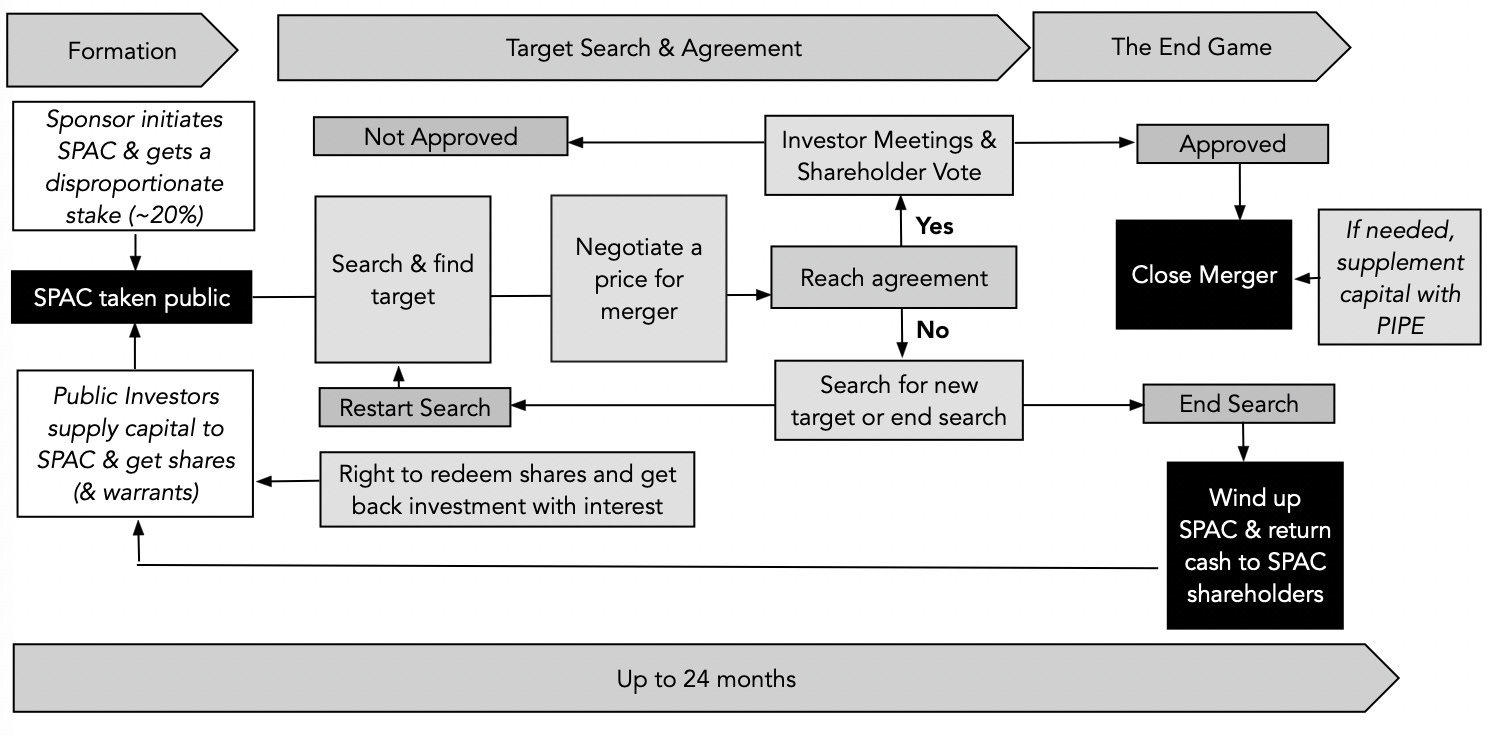

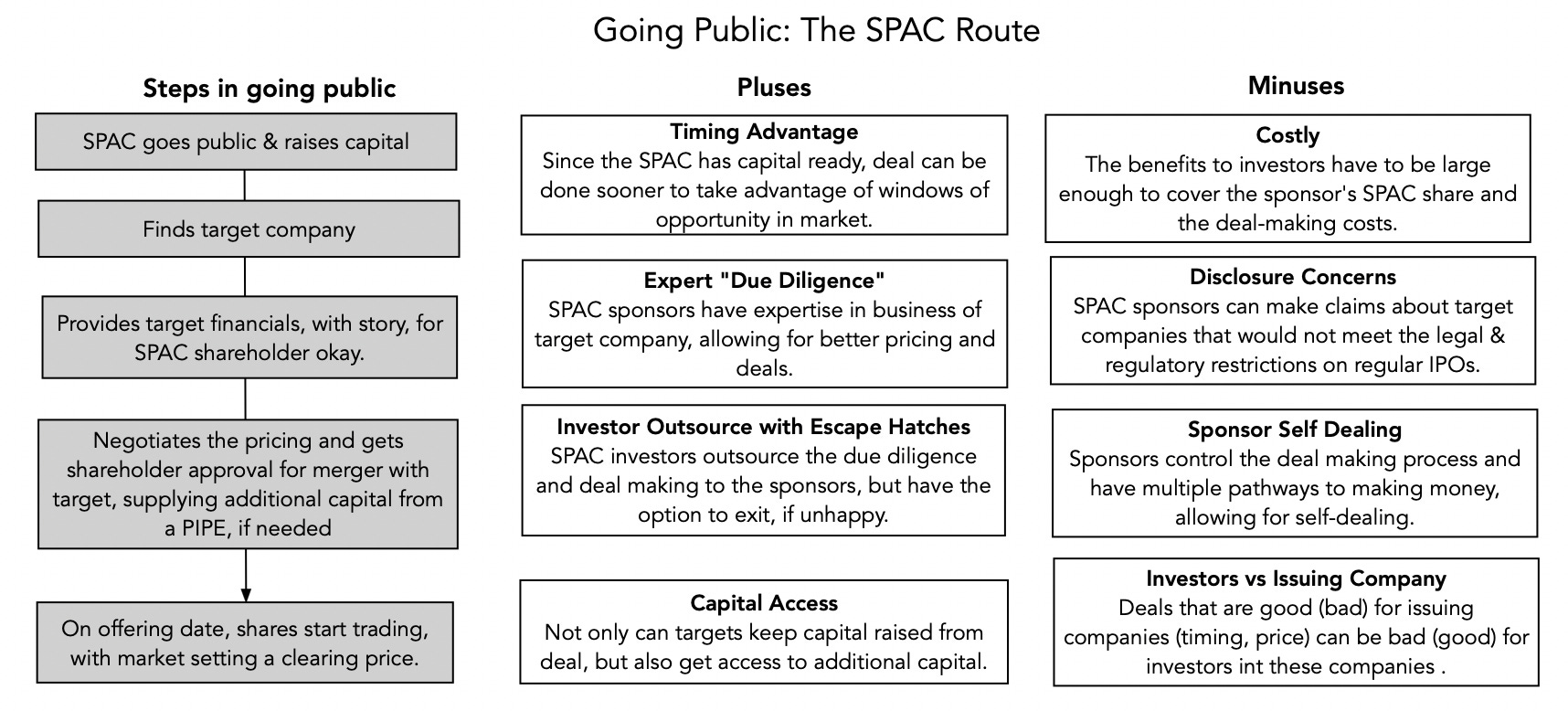

Aswath Damodaran talks SPACs

An incredibly detailed and insightful write up on SPACs in comparison to IPOs and Direct Listings. Aswath provides a good breakdown of what he dubs the SPAC effect for these listings. Worth the read for sure! It includes and goes into great detail about the charts below and renders some important findings between the different “go to market” options currently available.

Pandemic Hangover

The title of this article really says it all: "Pandemic Hangover: $11 Trillion in Corporate Debt"

It comes as no shock or news to the attentive finance reader that corporates turned to debt when interest rates collapsed during the COVID 19 pandemic. Stocks were down and profits were crumbling too, the only way to balance out the balance sheet was to load up on debt to meet current expenses.

What we have now is a new crossroad: was this debt dive a lucky opportunity for firms, or will firms be crushed when those debts come due? Sure, the interest rates were low when they locked in, but who's to say that these companies are going to be racking up enough EBIT to service those debt repayments (both interest and principal).

Notable quote: "The question now is whether companies have merely delayed a reckoning. Debt-laden companies withstood last year’s recession far better than many had feared. But it was in many ways a unique shock to the economy, more akin to a natural disaster than a typical recession. For all their current enthusiasm, many CFOs and investors acknowledge that businesses could still be punished in a normal downturn that raises borrowing costs for a longer period and does more serious damage to household finances."

How Crude!

Today (June 14), we saw a price level high for crude oil during the pandemic. What's behind this recent surge? Wall Street looks to be pricing in the upcoming push for green energy. This appears to be spooking investors in the energy space, shifting spending from oil extraction to production in greener methods of power production. The decrease in funding for extraction, investors are estimating, will cause a crunch on supply, bringing prices higher.

If we're seeing this artificial scarcity already (given that there is only an indication that the spending will be diverted), I can only imagine where markets will take prices in the future.

What I am reading now / plan to read

Here are some articles that I’ve saved and am making my way through in the last few days:

DraftKings: A $21 Billion SPAC Betting It Can Hide Its Black Market Operations - Hindenburg Research

I’ve not made my way through the whole report yet (it is quite long), but here are the summary bullets from the top of the report:

DraftKings has been considered one of the more successful deals in a recent wave of SPAC transactions marred by scandal and bad actors. Its stock is up ~398% from its announcement price.

The company went public in a 3-way merger between (1) DraftKings, (2) its SPAC sponsor, and (3) a Bulgaria-based gaming technology company called SBTech.

SBTech accounted for ~25% of total revenue at the SPAC consummation and was the only positive contributor to operating income, providing both financial stability and technology to the deal.

Unbeknownst to investors, DraftKings’ merger with SBTech also brings exposure to extensive dealings in black-market gaming, money laundering and organized crime.

Based on conversations with multiple former employees, a review of SEC & international filings, and inspection of back-end infrastructure at illicit international gaming websites, we show that SBTech has a long and ongoing record of operating in black markets.

We estimate that roughly 50% of SBTech’s revenue continues to come from markets where gambling is banned, based on an analysis of DraftKings’ SEC filings, conversations with former employees, and supporting documents.

As one former employee told us, DraftKings’ subsidiary SBTech has “sold to plenty of mobs”, a sharp contrast to the clean image of DraftKings’ brand-conscious partners, including the NFL, NBA, NASCAR, UFC and PGA, and the company’s recent hire of supermodel Gisele Bundchen to advise on governance issues.

Prior to the SPAC merger, SBTech seems to have made a concerted effort to distance itself from its black-market dealings. Illicit customer relationships were shuffled into a newly formed “distributor” entity called BTi/CoreTech, with ~50 SBTech employees shifted across town to the new entity.

The CEO selected to run BTi/CoreTech was formerly an executive of a ‘binary options’ gambling firm raided by the FBI and subsequently charged by the SEC for deceiving U.S. investors out of over $100 million.

Former SBTech employees called BTi/CoreTech a “front”, and said the split preserved SBTech’s (and now DraftKings’) illicit business while shielding the public company from scrutiny. For all practical purposes, it appears that BTi/CoreTech functions as DraftKings’ undisclosed illegal gaming division.

We identified numerous black market clients of DraftKings’ “front” entity, through searches on social media and back-end web infrastructure. For example, an Asia-focused site tied to a triad kingpin at the center of a Swiss money laundering investigation advertises its use of BTi/CoreTech technology.

In 2019, Vietnamese authorities arrested 22 individuals involved in a “massive illegal online sports betting ring” linked to BTi/CoreTech’s platform.

Contrary to representations made to Oregon’s state lottery, a former employee told us SBTech had extensive operations in Iran, violating local laws in a market subject to heavy U.S. sanctions. We were told SBTech knowingly operated there for 4-5 years with the founder directly overseeing the operation.

Around the time of the DraftKings deal, SBTech’s founder spun off another gaming brand that also operated in markets where gambling was banned, transferring it to his brother. The brand was behind a “massive Chinese operation”, according to a former employee, contrary to representations made to Oregon’s state lottery.

The brand continues to operate in China despite the strict local rules prohibiting online gambling, according to our review of web infrastructure for multiple China-facing gambling sites. DraftKings continues to transact with the entity, according to SEC filings.

DraftKings trades at a ~26x last twelve months (LTM) sales multiple and a ~20x estimated 2021 sales multiple despite (i) no expectation of earnings for years, (ii) intense competition, and (iii) regulatory risk. The company posted net losses of $844 million in 2020 and $346 million last quarter.

Insiders have dumped over $1.4 billion in stock since the company went public a little over a year ago, with SBTech’s founder leading the pack, having personally sold ~$568 million in shares.

Despite a rocky track record prior to taking DraftKings public, the company’s SPAC sponsors ultimately received 9.3 million shares, worth around $114 million at the time, in exchange for a token $25 thousand contribution.

We spoke with several industry experts and competitors who questioned the viability of DraftKings’ model of aggressively burning cash on promotion and marketing to acquire customers in the near term, despite a lack of evidence of long-term customer brand loyalty.

We think DraftKings has systematically skirted the law and taken elaborate steps to obfuscate its black market operations. These violations appear to be continuing to this day, all while insiders aggressively cash out amidst the market froth.

The Rise of Bankruptcy Directors - Jared Ellias

I just got my hands on this paper today, but am interested to dig into any new findings.

Abstract: In this Article, we use hand-collected data to shed light on a troubling innovation in bankruptcy practice. We show that distressed companies, especially those controlled by private-equity sponsors, often now prepare for a Chapter 11 filing by appointing bankruptcy experts to their boards of directors and giving them the board’s power to make key bankruptcy decisions. These directors often seek to wrest control of self-dealing claims against shareholders from creditors. We refer to these directors as “bankruptcy directors” and conduct the first empirical study of their rise as key players in the world of corporate bankruptcy. While these directors claim to be neutral experts that act to maximize value for the benefit of creditors, we argue that they suffer from a structural bias because they are part of a small community of repeat private-equity sponsors and law firms. Securing future directorships may require pleasing this clientele at the expense of creditors. Consistent with this prediction, we find that unsecured creditors recover on average 21% less when the company appoints a bankruptcy director. While other explanations are possible, this finding at least shifts the burden of proof to those claiming that bankruptcy directors improve the governance of distressed companies. Our policy recommendation, however, does not require a resolution of this controversy. We propose that the court regard bankruptcy directors as independent only if all creditors support their appointment, making them accountable to all sides of bankruptcy disputes.

Exclusive: Daniel Kamensky Speaks. Part I and Part II. 🔥🔥 - PETITION

Part I and Part II can be found and read with care here or in the Twitter threads below. You already know PETITION brings the heat.

The Economic Question of Our Time - Heisenberg Report

Just read the whole piece; it is well worth your time. For the lazy folks, here is the knockout punch:

Ultimately, I doubt there’s much of a middle ground between things going “wrong” and things going “right” as described above. Either conventional wisdom on inflation is antiquated or it’s not. I tend to believe it is for two reasons.

First, virtually everyone admits there’s no reliable model for inflation. It’s not clear (at all) that any of the Fed’s multitudinous critics have a better model than policymakers. Saying someone else’s model doesn’t work isn’t the same as saying yours does.

Second, and more importantly, I think things are now so complex, that the average consumer, no matter how intelligent, simply doesn’t have time to make a mental sketch of the path to a long-term surge in inflation. Everyday people understand supply and demand intuitively. But their interest in ratios like that shown in the third figure (above) is de minimis.

Please let me know what you think of this new style. I really enjoy posting on Bookshlf. The community over there is strong, and I’ve gained a strong readership over there. The social media site itself is growing and tends to lend itself nicely to honestly curated and factual information.

I plan to keep this newsletter refreshing with different styles and reporting methods. I was complacent for too long but am excited for this next chapter.

Well done. You’ve made it through the madness. I’ve worked hard to ensure that you leave this page having learned something, and I hope that it benefits you in your daily adventure. Thank you again for checking in.

[Market Madness] Edition 0144